- Maritime Data Newsletter

- Posts

- What are the current and potential risks to commodity markets from the ongoing crisis in the Red Sea? 🚢 The implications on Global Seaborne Trade 🌍 and how to navigate the latest Global Supply Chain Disruption 🔄

What are the current and potential risks to commodity markets from the ongoing crisis in the Red Sea? 🚢 The implications on Global Seaborne Trade 🌍 and how to navigate the latest Global Supply Chain Disruption 🔄

Rory Proud

February 02, 2024

Maritimedata.ai is a digital broker that provides data and analytics solutions for the maritime ecosystem.

Source, evaluate and purchase maritime data and analytics from the largest network of specialised providers in the world.

The newsletter provides you with up-to-date information on the most recent advancements in space and market insights produced by partners in the Maritime Data network.

Insights 📈

Oil

Dry Bulk

Other

Red Sea 🌊

Ten incidents of hijacking in Somalia’s territorial waters Maritrace

Red Sea Update: Charterers Reassess Risk And Trade Lanes Shift Lloyd’s List Intelligence

Red Sea AIS Guidance, Dark Activity Spike, and the Area You Can’t Ignore…Windward

Red Sea Update: Global LR fleet most affected, while Russia-origin oil continues to transit Vortexa

Navigating the Latest Global Supply Chain Disruption Dun and Bradstreet

What are the current and potential risks to commodity markets from the ongoing crisis in the Red Sea? Kpler

CO2 Surge at Sea: The Environmental Toll of Redirection in Maritime Routes Amid Red Sea Crisis Portcast

The Red Sea Escalation: Implications on Global Seaborne Trade Signal

Meet our new Partner

Geospatial analysis and intelligence

A UK Leader in Geospatial intelligence technologies, Geollect serve both the Maritime and Defense markets with insights derived from their unique approach that combines human expertise with advanced technology, harnessing the power of AI, machine learning, and sensor technology.

Ten incidents of hijacking in Somalia’s territorial waters Maritrace

Amid ongoing threats to commercial shipping in the Red Sea and increased maritime security risks in the Gulf of Aden, ten incidents of hijacking in Somalia’s territorial waters and in the Arabian Sea since November 2023 have revitlised concerns about the return of Somali Piracy, previously believed to have all but ceased.

Given the large number of commercial ships that transit the area on approach to the Gulf of Aden, regional counter-piracy authorities and shipping companies and attentive to the recent increase in hijacking incidents. Some are concerned this may signal a further phase of heightened security risks to commercial shipping.

As at January 30 2024, the recent phase of incidents have occurred in five clusters:

Near to Qandala, on the northern shores of Puntland.

Near to Al Hafun, on Somalia’s eastern coast

Near to Eyl, on Somalia’s eastern coast

Offshore, east of the island of Socotra

Offshore, 400 - 600 NM (approx 900 km) east of Puntland

Organisnig an effective response will rely on rapid information sharing, stability of maritime cooperation mechanisms established before the advent of threats to shipping in the Red Sea and Gulf of Aden and renewed attention to the factors on land that are motivating and enabling criminal networks to self-organise and take advantage of opportunity at Sea.

Ten incidents of hijacking in Somalia’s EEZ and the Arabian Sea since November 2023 have renewed concerns about the threat of piracy. Source: Maritrace

Red Sea Update: Charterers Reassess Risk And Trade Lanes Shift Lloyd’s List Intelligence

Key data from Lloyd’s List Intelligence for the week ending January 28, 2024:

The number of cargo-carrying active vessels (10,000dwt+) that are not berthed or anchored in the Red Sea fell to 199 in the week ending January 28, down from 221 last week and 366 in the corresponding week last year.

The number of cargo-carrying vessel (10,000dwt+) transits through the Suez Canal is down 16% week on week and down 45% compared to the same week in 2023.

Cargo-carrying vessel (10,000dwt+) transits around the Cape of Good Hope are up 4% from last week and 78% higher year-on-year.

Tanker operators are rerouting vessels away from the Red Sea in the wake of a Houthi attack which left a Trafigura-chartered vessel in flames over the weekend.

The weekly daily average of active ships in the Red Sea was 229, down from 255 the week prior and down from 367 over the same period last year.

Source: Lloyd’s List Intelligence / Seasearcher

Note: Only includes cargo-carrying vessels over 10,000 dwt that are not berthed or anchored

Red Sea AIS Guidance, Dark Activity Spike, and the Area You Can’t Ignore…Windward

Another Follow-the-Leader Effect?

Two vessels near the Gulf of Aden were forced to seek the support of the U.S. Navy after explosions occurred nearby on Wednesday. No damage was caused to the Maersk Detroit or Maersk Chesapeake.

“Following the escalation of risk, (Maersk Line, Limited) MLL is suspending transits in the region until further notice,” it said on Wednesday.

We saw a follow-the-leader effect a month ago after the world’s largest carrier announced it would avoid the Red Sea. Expect another wave of supply chain disruption – there were still 32 UK and U.S. vessels transiting the area this past month, according to Windward’s Maritime AI™ platform.

Clusters of the UK and U.S. vessels from Windward’s Maritime AI™ platform

This recent incident, coupled with earlier ones (see below), will further drive insurance premiums up and create even more disruptions as a greater number of charterers and carriers avoid the area. Freight and insurance rates will continue to rise…

Trade flows are changing, which is why we launched our new Sequence Search. It’s a unique way for users to conduct advanced analysis of vessels’ behavioral typologies and trade movements by searching for a sequence of activities. It also helps contextualize the journey, enabling users to see if route deviations were conducted for security reasons, or for concealing illicit activities.

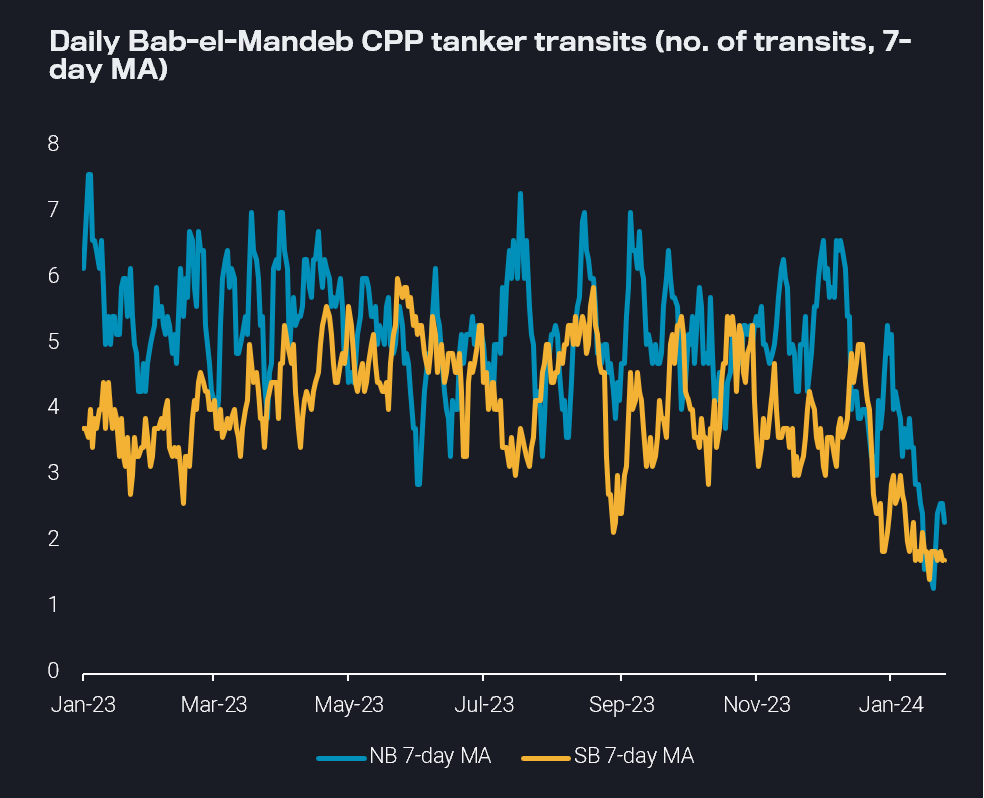

Red Sea Update: Global LR fleet most affected, while Russia-origin oil continues to transit Vortexa

LRs and the outsized impact from Red Sea attacks

Clean tanker transits via the Bab-el-Mandeb have continued to decline since Red Sea attacks on non-Israeli vessels began mid-December. Southbound transits have largely stopped, hovering at slightly over one transit per day on a moving average basis. CPP volumes still going through are almost all Russian-origin heading East. Northbound CPP tanker transits slightly recovered going into the New Year but declined precipitously following the US/UK-led strikes on 12 January. Some tankers were initially adopting a ‘wait and see’ approach in the Arabian Sea, but virtually all have now made the decision to divert around the Cape of Good Hope (COGH).

Daily Bab-el-Mandeb CPP tanker transits (7-day MA, no. of transits) (Retrieved via Freight API/SDK)

Navigating the Latest Global Supply Chain Disruption Dun and Bradstreet

The Red Sea disruption has escalated to alarming levels, with naval attacks, counterstrikes, and shipping carriers avoiding the area. It is of utmost urgency for businesses to assess the impact on critical inventory and take immediate action.

Dun & Bradstreet Shipping Insights offers a crucial tool to interpret the rapidly changing global shipping landscape in light of these developments. The Red Sea is a vital shipping route connecting one end of the Suez Canal. According to D&B Shipping Insights data, it is bordered by six sovereign nations, with five actively engaged in shipping: Egypt, Eritrea, Israel, Sudan, and Yemen. These countries host 55 active shipping ports, previously showing increasing shipping activity. However, recent events have led to a significant decline in shipping activity, particularly with vessels bearing an Israeli flag experiencing a devastating decrease of over 66% year over year.

The repercussions of the Red Sea attacks extend far beyond Israel, impacting businesses on a global scale. Three immediate outcomes directly affect shipping through the area. Firstly, insurance premiums have skyrocketed by over 3500%, putting additional financial strain on businesses, according to reports published by NPR. Secondly, alternative routes must be considered, resulting in additional costs incurred. Lastly, extended delivery times are causing adjustments to expectations, leading to potential customer dissatisfaction and operational challenges.

What are the current and potential risks to commodity markets from the ongoing crisis in the Red Sea? Kpler

Overview

As the disruption around the Bab el-Mandeb strait enters its third month, a rising number of bulk vessels are avoiding the region, creating ever broader negative impacts to commodity markets and the wider economy. To counter the threat, the US and UK conducted coordinated strikes on Houthi targets in Yemen earlier this month. This has not deterred the Iran backed Houthis with attacks on vessels persisting, most recently with a strike on the tanker Marlin Luanda carrying Russian naphtha, the most serious attack on a vessel to date.

Average daily Suez Canal transits by bulk commodity carriers hit a more than two-year low of 28 on 26 January. The recent strike on the Marlin Luanda highlights the ongoing risk to vessels and the likelihood that the current crisis will impact shipping and commodity markets for the foreseeable future. In this report, we highlight the current and potential risks to various commodity markets.

Macroeconomic

Escalating tensions in the Red Sea represent a risk to global disinflationary trends we've seen over the past year. Containership flows through the Red Se, in particular, have eased considerably with numerous containership firms, including Maersk, banning all Red Sea shipments indefinitely. This effectively pushes up the cost to ship goods from east to west amid longer transit times around the Cape of Good Hope. Higher freight costs are effectively passed through to goods prices. Europe is the most exposed to rising costs due to its dependence on imports from Asia. The cost of manufactured goods from clothing to furniture is expected to jump in March and if issues persist in the Red Sea, rising prices could be a longer-run structural problem. Other regions, such as the United States, could also begin to feel knock-on effects as higher freight rates between Asia and Europe spread further afield.

Geopolitical

Houthi actions in the region enjoy full Iranian backing. Tehran derives three primary benefits from these events:

A potential upward push on oil price

Disproportionately higher costs for the US and the UK in intercepting Houthi missile

An enhancement of its reputation in the Muslim and Arab world. Notably, a recent survey by the Doha Institute indicates a shift in perception, with the Arab world now viewing the US and Israel as the major threats to peace and stability in the region, providing Tehran with a significant political advantage.

Moreover, recent events, including Iran's seizure of the Suezmax vessel St Nikolas in the Gulf of Oman, pose additional risks to the freight market. The St Nikolas was laden with Basrah crude destined for Tupras’ Aliaga refinery. This incident, distinct from Houthi activity near the Gulf of Aden, has triggered potential consequences in the Iran-Turkey-Iraq relationship. Iran alleges that the vessel owner and the US had 980 kb of Iranian crude stolen last year, originally transported within the same vessel but eventually diverted and delivered to the US.

CO2 Surge at Sea: The Environmental Toll of Redirection in Maritime Routes Amid Red Sea Crisis Portcast

The Red Sea attack crisis has led to continued rerouting of vessels through the Cape of Good Hope, which has not only altered the dynamics of global shipping but has also unveiled an environmental consequence —a surge in carbon emissions.

Earlier, when the crisis started, and the vessels started rerouting, Portcast predicted and informed about the possible increase in carbon emissions, specifically focusing on the South Asia region (India/Colombo) to Europe and the US East Coast.

South Asia Region to Europe: A 50% Surge in CO2 Emissions

Traditionally, vessels from South Asia to Europe have relied on the Suez Canal, a critical shortcut that significantly reduces travel distances and emissions. Portcast's calculations reveal a staggering 50% increase in carbon dioxide emissions for shipping between the South Asia region and Europe.

South Asia Region to US East Coast: A 20% Rise in CO2 Emissions

The impact is not confined to the European routes alone; vessels between the South Asia region and the US East Coast have also experienced a notable increase in carbon emissions.

Portcast's data indicates an approximate 20% surge in CO2 emissions for shipping between the South Asia region and the US East Coast.

Impact of Redirection on Critical Routes

Recent findings from Portcast shed light on the stark increase in CO2 emissions for shipping routes between China, Singapore, Malaysia, and Europe, as well as the US East Coast.

Singapore/Malaysia to Europe: CO2 emissions increased by 40%.

Singapore/Malaysia to US East Coast: CO2 emissions rose by 16%.

China to Europe: CO2 emissions saw a 30% increase.

China to US East Coast: CO2 emissions increased by 12%.

[Note: Various factors influence CO2 emissions, and these figures represent a general trend observed by Portcast.]

The Red Sea Escalation: Implications on Global Seaborne Trade Signal

In recent days, discussions have intensified about the potential impact on the seaborne trade and ton-miles due to the evolving dynamics of market spot rates in various shipping segments. The recent attacks by the Houthi rebels in the Red Sea have already started to significantly affect trading activities, especially in the container segment. With the start of the new year, the crisis now appears to be impacting Red Sea vessel counts in the crude tanker segment, while spot rates in the Atlantic routes have spiked and piqued the interest of the market, signalling an escalation of the crisis with daily occurrences of new attacks.

In the dry bulk segment, the market has not experienced a significant impact yet. However, as time progresses, the threat of Houthi attacks on both dry and wet seaborne trade appears to be escalating. Figure 1 below, examines which segments were the most exposed to Suez canal crossings in 2023. Suezmax and Aframax and Supramax and Panamax represent more than half of the total crossings in tankers and dry bulk respectively.

Figure 1: % of Voyages that ended in 2023 with a Suez canal crossing per Vessel Class, Tanker & Dry

How we can help

A member of the team will reach out within 24 hours

Explore which of our 200+ data and analytics solutions can support you

Start receiving enquiries and meeting new clients

You might be receiving this email because we believe that the content of our newsletter may be of interest to you based on your profession. However, if we have made an incorrect assumption, we apologize for any inconvenience caused. If you do not wish to receive future publications, please follow the instructions below to unsubscribe.

Thank you for your time.

Best regards,

Rory Proud

Co-Founder